What can be the next breakthrough in Indian economic reforms history?

a TAX system that,

- technically is a next generation tax system, that scopes all direct & indirect taxes as a single tax system with exception of customs duty.

- supports auto tax compliance to individuals (i.e., IT return submission not needed anymore).

- simplifies tax compliance to all kinds of organizations (i.e., commercial/non-commercial/other).

- fosters start-ups ecosystem.

- stimulates domestic investments & FDI.

- brings-in accountability with NGOs, political parties, funds etc…

- supports fulfillment of all practically considered & viable budgetary commitments, while accommodating future opportunities in a fiscal surplus position.

- funds public good services like UPI, similar to public education, libraries, healthcare centres, sanitation, street lighting, law enforcement, fire protection, infrastructure maintenance (roads, bridges, communications networks, etc..), national defense, clean drinking water etc….

- is a real-time tax collection system by nature, that has provision to also “reverse charge” tax from customers w.r.t. cash transactions.

About Budget of FY 2022-23:

Union Budget for FY 2022-23 that was presented on 01 Feb 2022 is: Rs.39.45 lakh crores.

Tax system alternative of incumbent tax systems:

Non-Cascading Transaction Tax, a unique variation of transaction tax concept, has all the features as described above, to serve as a potential replacement of incumbent tax systems like Income Tax (direct tax), GST (Indirect tax) and Property Tax (direct tax).

For more details on Non-Cascading Transaction Tax Proposal, please visit:

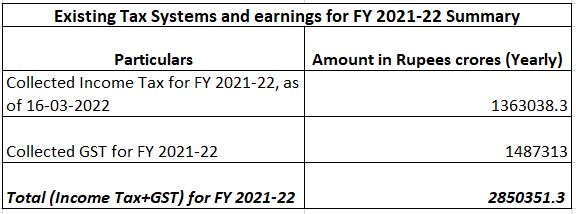

Potential tax collection calculation based on publicly available data:

This shows a potential possibility of 4X growth in budgeted expenditure and 5.5X growth with revenue and capital receipts.

Points to be considered for improving accuracy in Transaction Tax calculations:

The following are some of the parameters/criteria that needs attention, that will have incremental (+) and decremental (-) effect on the total tax collection scope in Non-Cascading Transaction Tax regime, that were documented in the following,

Incremental (+) / additional tax revenue to the tax department:

- IMPS transaction value for FY 2022-23 with projections (in-direct tax scope).

- Cash payments in FY 2021-22 (in-direct tax scope).

- Salary received as cash in FY 2021-22 (direct tax scope).

- Tax amounts to be enumerated for sectors/industries like mining, sea port charges, toll gate fee etc… to be enumerated as applicable.

Decremental (-) to tax department but, that covers refunds, Input Tax Credit etc… to tax payer:

- Amount that has to be reduced to remove tax amount that might have been considered in the above, in the scope of cascaded transactions in business and individual scopes as per non-cascading transaction tax proposal.

Note: This is a tough job as checking the purpose of the transaction and identification of the nature of the transaction in terms of if it is cascading or not might be a difficult/tedious task, post the transaction. - Amount that can be claimed by businesses as Input Tax Credit, post submission of the tax returns (similar to GST regime).

- 100% tax amount that can be claimed as refund, by NGOs, Spiritual Organizations, Political Parties, Funds etc…, post submission of the tax returns.

Summary:

Tax is among the primary sources of revenue to governments, in most of the countries across the world. While India is not an exception, adopting proportional tax systems like GST (that is also considered to be an indirect tax system), is something that is required to fund India’s infra investments and many other initiatives. On other hand, India has progressive tax systems in the scope of income tax & property tax (that is also considered to be direct tax system), that is also generating revenue to the government.

India/Bharatavarsha is a rapidly growing country and choosing a proportional tax system over the prevailing progressive tax systems of all kinds, in it’s entirety, that has direct tax & indirect tax components, is a very much needed decision that can enable India to invest on human resources (by providing quality education and healthcare to all citizens & residents) on one side and on infrastructure and other initiatives on the other, while offering the current & future generations a level playing field, with any opportunity they choose to explore & excel in, facilitating them to create their page in India/Bharatavarsha’s growth story and in making India, a product nation once again.